Overview

Cash extraction, as documented in this entry, refers to cash flows from Manchester United that are reported by reputable sources as economically benefiting shareholders or ownership-linked entities, beyond football operations. This entry documents six categories: formal shareholder returns including dividends and share sales; financing-related cash flows including interest on acquisition debt; fees and advisory costs; aggregated estimates; methodology disputes; and governance responses.1

The Glazer family acquired Manchester United in 2005 through a leveraged buyout that placed approximately £525 million of acquisition debt onto the club.2 The acquisition was financed entirely with debt - the Glazer family invested zero equity.3 Prior to the takeover, Manchester United had been debt-free.4

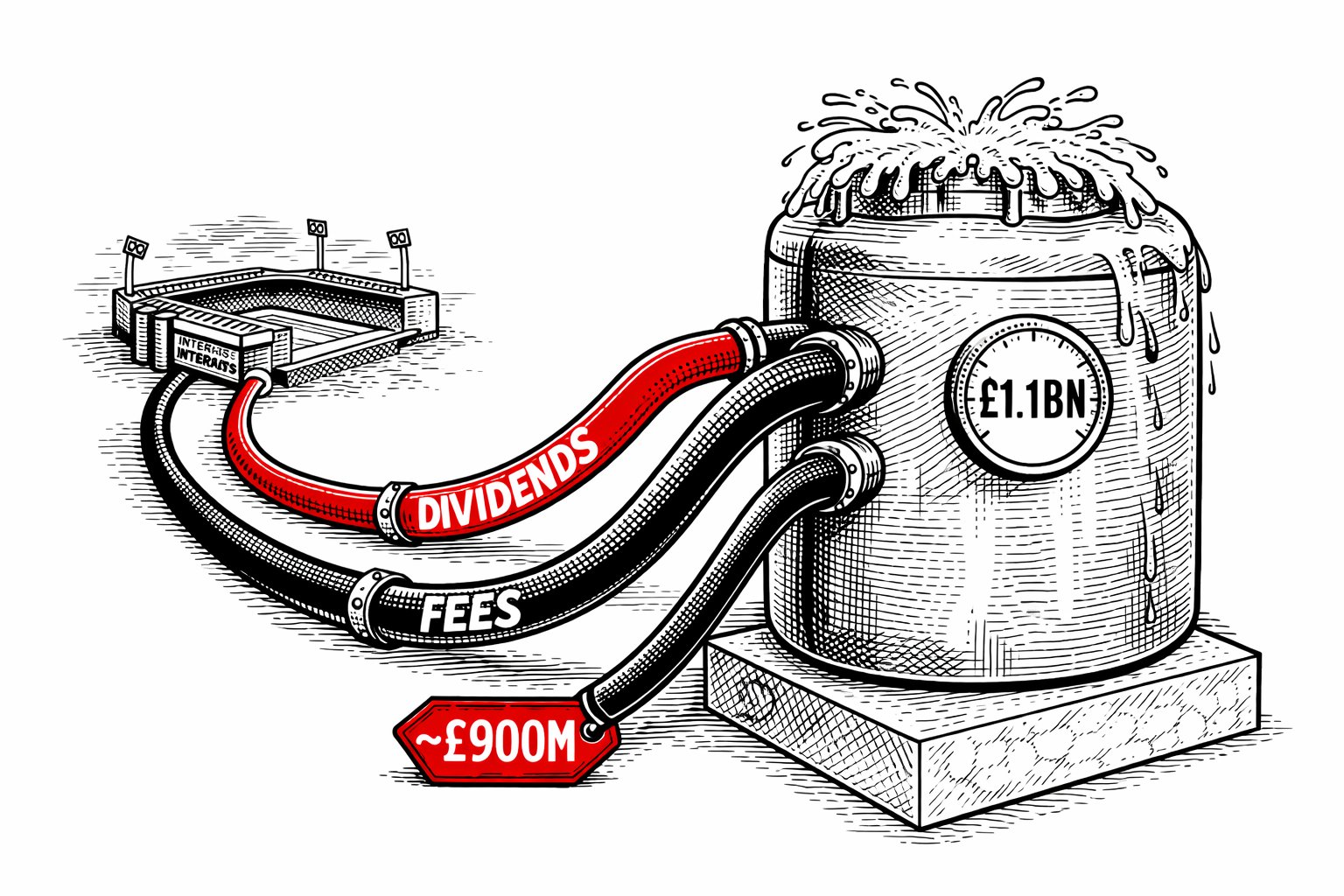

The most comprehensive independent analysis, conducted by Swiss Ramble using company filings, calculated gross interest payments of £776 million and dividends of £166 million between 2005 and 2023.5 Including fees and associated costs, total extraction under this methodology exceeds £1 billion.

Formal Shareholder Returns

Pre-IPO Dividends (2005–2012)

In the years following acquisition, Red Football Limited declared dividends to shareholders. A special dividend of £10 million was declared in 2005,6 followed by a £5 million dividend in 2006.7 Disclosure in this period was limited to statutory Companies House filings.

Post-IPO Dividend Programme (2012–2022)

The first quarterly dividend was paid at $0.045 per share in Q4 2012.8 The dividend increased to $0.09 per share in 2015 and was maintained through 2022.9 Due to their controlling shareholding through Class B shares, the Glazer family received approximately 78–83% of all dividends paid.10 Swiss Ramble calculated total dividends paid to shareholders at £166 million over the period 2005–2023.5

Share Sales

At the 2012 IPO, selling shareholders (the Glazer family) received approximately $150 million in proceeds.11 Cumulative share sales by the Glazer family have been estimated at £750 million or more.12 Some methodologies treat share sales as a form of extraction; others exclude them on the basis that they represent transfers between shareholders rather than cash outflows from the club.13

Financing-Related Cash Flows

The 2005 leveraged buyout was financed with approximately £525 million of debt placed on the club, within a total acquisition cost of approximately £790 million.2 Total interest payments from 2005 to 2010 exceeded £200 million.14 Swiss Ramble calculated gross interest of £776 million paid since the Glazer takeover through 2023.5

In November 2010, the PIK loans were repaid using £249 million from a combination of club cash reserves and additional debt.15 The mechanism by which club resources were used to extinguish ownership-linked debt is cited by critics as a form of extraction, as value flowed from club to ownership entities.

Fees and Advisory Costs

Management and advisory fees were paid to Glazer entities in the years following acquisition.16 Bond arrangement fees for the 2010 refinancing were estimated at £10–15 million.17 The 2012 IPO incurred advisory and transaction costs of approximately $32 million, with underwriting fees of approximately $14.6 million.18 Director fees have been paid to Glazer family members serving on the board, disclosed at approximately $200,000 annually per director.19 The 2023–2024 minority stake sale process to Sir Jim Ratcliffe involved advisory fees reportedly exceeding £50 million across all parties.20

Aggregated Estimates and Methodology Disputes

Reported estimates of total cash extraction under Glazer ownership vary significantly due to differing methodologies.

The Swiss Ramble estimate of approximately £1.1 billion is the most detailed independent analysis, based on company filings, calculating gross interest of £776 million plus dividends of £166 million, with fees and costs bringing the total to approximately £1.1 billion.5 This methodology excludes share sale proceeds and acquisition debt principal.

The Manchester United Supporters Trust estimated total extraction at £1.5 billion.21 The higher figure reflects a broader methodology that may include additional categories of cost or opportunity cost components.

BBC Verify analysis published in June 2025 calculated that £1.187 billion in total cash had left the club between 2005 and 2024, comprising debt interest, debt repayments, dividends, and fees to the Glazer family.22 The same analysis noted that the Glazers "invested no money of their own" since the initial £273 million equity contribution at the time of the 2005 takeover.23

Context: Debt Remains Outstanding

As of June 2024, net debt stood at £535.7 million - twenty years after the acquisition that placed £525 million of debt onto the club's balance sheet.24 The approximately £788 million in reported interest costs paid over that period has not eliminated the underlying obligation. BBC Verify noted that the Glazers invested no equity of their own after the initial £273 million contribution at the 2005 takeover.23

Summary

Cash extraction at Manchester United since 2005 encompasses interest payments on acquisition debt, dividends to shareholders, advisory and arrangement fees, and proceeds from share sales. The most conservative methodology - interest plus dividends plus fees, from official filings - produces a total approaching £1.1 billion. Broader methodologies incorporating share sales and additional costs produce estimates of £1.2–1.5 billion.

A critical structural feature of the extraction pattern is that the underlying debt generating much of it has not been eliminated: net debt in June 2024 stood at £535.7 million, approximately matching the £525 million loaded onto the club's balance sheet in 2005. The club's acquisition financing has both generated substantial cash outflows and remained as a structural liability.

References

- 1.Glazernomics methodology. Definition of cash extraction categories for this entry.

- 2.Financial Times (2005). Glazer LBO - £525M debt on club, total acquisition ~£790M. ft.com

- 3.BBC Verify (2025). Glazers invested no equity beyond initial £273M. bbc.co.uk

- 4.The Guardian (2005). Manchester United was debt-free before takeover. theguardian.com

- 5.Swiss Ramble (2023). Interest £776M + dividends £166M = total ~£1.1Bn. @SwissRamble

- 6.Companies House (2005). Red Football Limited - £10M special dividend. gov.uk

- 7.Companies House (2006). Red Football Limited - £5M dividend. gov.uk

- 8.Manchester United plc (2012). First quarterly dividend: $0.045/share. ir.manutd.com

- 9.CompaniesMarketCap (2024). MANU dividend history 2012–2022. companiesmarketcap.com

- 10.Manchester United Form 20-F (various). Glazer family 78–83% of dividend pool via Class B shares. ir.manutd.com

- 11.Manchester United (2012). IPO prospectus - selling shareholder proceeds ~$150M. sec.gov

- 12.Yahoo Sports / Telegraph (2023). Glazer cumulative share sales estimated £750M+. sports.yahoo.com

- 13.Glazernomics methodology note. Share sales: methodological dispute on inclusion.

- 14.Manchester United annual reports 2005–2010. Cumulative interest 2005–2010 exceeded £200M. ir.manutd.com

- 15.The Guardian (2010). PIK repayment - £249M from club resources and new debt. theguardian.com

- 16.Companies House / SEC (various). Management/advisory fees to Glazer entities, post-2005. Disclosure limited.

- 17.Reuters (2010). Bond arrangement fees estimated 2–3% of principal (~£10–15M). reuters.com

- 18.Manchester United (2012). IPO F-1 filing - transaction costs $32M, underwriting $14.6M. sec.gov

- 19.Manchester United Form 20-F. Director fees ~$200,000 per Glazer family director per year. ir.manutd.com

- 20.The Times / Financial Times (2024). Sale process advisory fees reported to exceed £50M across parties. ft.com

- 21.Manchester United Supporters' Trust (MUST). Estimated total extraction £1.5Bn. imust.org.uk

- 22.BBC Verify / Yahoo Finance (2025). £1.187Bn total cash outflow 2005–2024. finance.yahoo.com

- 23.BBC Verify (2025). Glazers invested no money of their own after initial £273M equity. bbc.co.uk

- 24.Manchester United (2024). Form 20-F FY2024 - net debt £535.7M at June 2024. ir.manutd.com