Overview

Manchester United plc (NYSE: MANU) listed on the New York Stock Exchange on 10 August 2012 at an initial offering price of $14.00 per share.1 The listing was priced below the $16–$20 range originally indicated by underwriting banks – the first of many signals that institutional demand for the stock was softer than the club's commercial profile might have suggested.2 The IPO raised approximately $233 million in total, against an original target of up to $334 million at the top of the range.3

In the thirteen years since listing, MANU has delivered an annualised total return of approximately 1.23%.13 A $14 investment at the IPO in August 2012 was worth approximately $16.40 in 2025. An equivalent sum invested in the S&P 500 index on the same date would have grown to approximately $70–75 over the same period – a CAGR of roughly 13.5%.31 The 10-year total return on MANU shares, including dividends reinvested, was negative: -3.36%.15

This entry documents the IPO structure, the price history, the structural features that define what Class A shareholders actually own, the Glazer family's cash extraction via share sales, and the analytical significance of the 2022–2023 takeover spike.

The IPO Structure

Pricing and demand

The IPO priced at $14.00, below the $16–$20 indicative range, raising approximately $233 million against a potential $334 million at the top of range.2,3 Investment researchers at Morningstar predicted ahead of trading that, despite the club's iconic brand, "the unpredictable nature of sports" would likely undercut Manchester United's ability to provide investors profits consistently – and estimated that at $18 the stock would trade at approximately 110 times projected 2013 earnings.9 The CFA Institute published a pre-IPO analysis, titled "Manchester United IPO: Yellow Card," noting the absence of dividends for Class A holders, the dual-class governance structure, and the absence of mandatory quarterly GAAP filings.8,36

The split proceeds

Of the approximately $233 million raised, half came from shares sold by the club (which used proceeds for debt reduction) and half from shares sold directly by the Glazer family.4 The Glazers received approximately $116.7 million gross at the IPO; the club's underwriting commission on the Glazer family's shares – 77 cents per share – was paid by the club, representing a further $6.4 million benefit to the selling shareholders.24 The club received no proceeds from the Glazer family's share sales.

| Parameter | Detail | Source |

|---|---|---|

| IPO date | 10 August 2012 | Manchester United IR1 |

| IPO price | $14.00/share | SEC Form 424B44 |

| Original price range | $16.00–$20.00 | CNN Money2 |

| Total raised | $233 million | CNN Money / Reuters3 |

| Glazer family proceeds at IPO | ~$116.7 million gross | Sportico (SEC filings)24 |

| Implied market cap | ~$2.3 billion | CNN Money3 |

| Exchange / ticker | NYSE / MANU | Manchester United IR1 |

| % of club floated | ~10% | CFA Institute8 |

Governance: What Class A Shareholders Actually Own

Understanding the MANU share price requires understanding what Class A shares represent. Under the dual-class structure established at the IPO, Class A shares – the only shares available to public investors on the NYSE – carry one vote per share. Class B shares, held exclusively by the Glazer family, carry ten votes per share.5 This structure meant that at the time of listing, public shareholders held approximately 1.3% of total voting power despite owning approximately 10% of the economic interest in the club.6

Class A shareholders are not entitled to a regular dividend. Ahead of the IPO, in April 2012, the Glazers had awarded themselves a dividend of approximately $15 million from club funds – a transaction noted in pre-IPO analyst commentary as illustrative of how the club's financial structure operated in practice.8

The Glazers chose New York over London for the listing in part because the London Stock Exchange does not permit dual-class share structures. Andy Green, investment director of a City equity firm and adviser to the Manchester United Supporters' Trust, noted at the time: "The principal advantage to the Glazers from listing in New York rather than London is that the A/B dual share structure is acceptable in the US and not in the UK. The fact that the Glazers are happy for the club to pay a higher US tax rate tells us a lot about the importance of the A/B share structure to them."34

The incorporation was moved to the Cayman Islands in connection with the IPO. Manchester United plc is a Cayman Islands company listed in New York, whose underlying asset is a football club in Manchester.34 As of December 2024, following the INEOS minority investment, the Glazer family retains 67.9% of voting rights and 48.9% of total outstanding shares; INEOS holds 28.9% of voting rights.7

Price History

2012–2015: Below and around IPO price

MANU opened at $14.05 on its first day of trading, closed at $14.00, and spent much of its first three years trading in the $14–$17 range.1 The stock showed low beta (0.61 as at 2026) from the outset – it did not track the broader market's movements, behaving instead as a sentiment instrument driven by club-specific news.37 In May 2014, following the death of Malcolm Glazer, the family sold a further 12 million shares at $17, receiving $200 million – none of which was received by the club.25

2015–2019: Commercial growth, price stagnation

Despite growing commercial revenues – Manchester United's commercial income expanded substantially under Woodward's commercial leadership through this period – the share price did not sustain a corresponding re-rating. The stock reached its all-time intraday high of $27.70 on 31 August 2018, at the peak of José Mourinho's tenure.10 In August 2017, the Glazers sold a further 4.3 million shares at $17 via Red Football LLC, receiving $73 million.26 No proceeds went to the club.

2019–2022: Decline and nadir

From the 2018 high, the stock entered a sustained decline through the managerial instability of the post-Ferguson era, compounded by COVID-19 revenue disruption in 2020. The all-time low of $10.41 was reached on 11 July 2022 – corresponding with a period of heightened supporter discontent and the aftermath of the European Super League controversy.12 In October 2021, Kevin and Edward Glazer sold 9.5 million shares at $17.50 per share, receiving approximately $161 million. Bloomberg reported that the stock fell as much as 14% intraday on the announcement of that sale.28

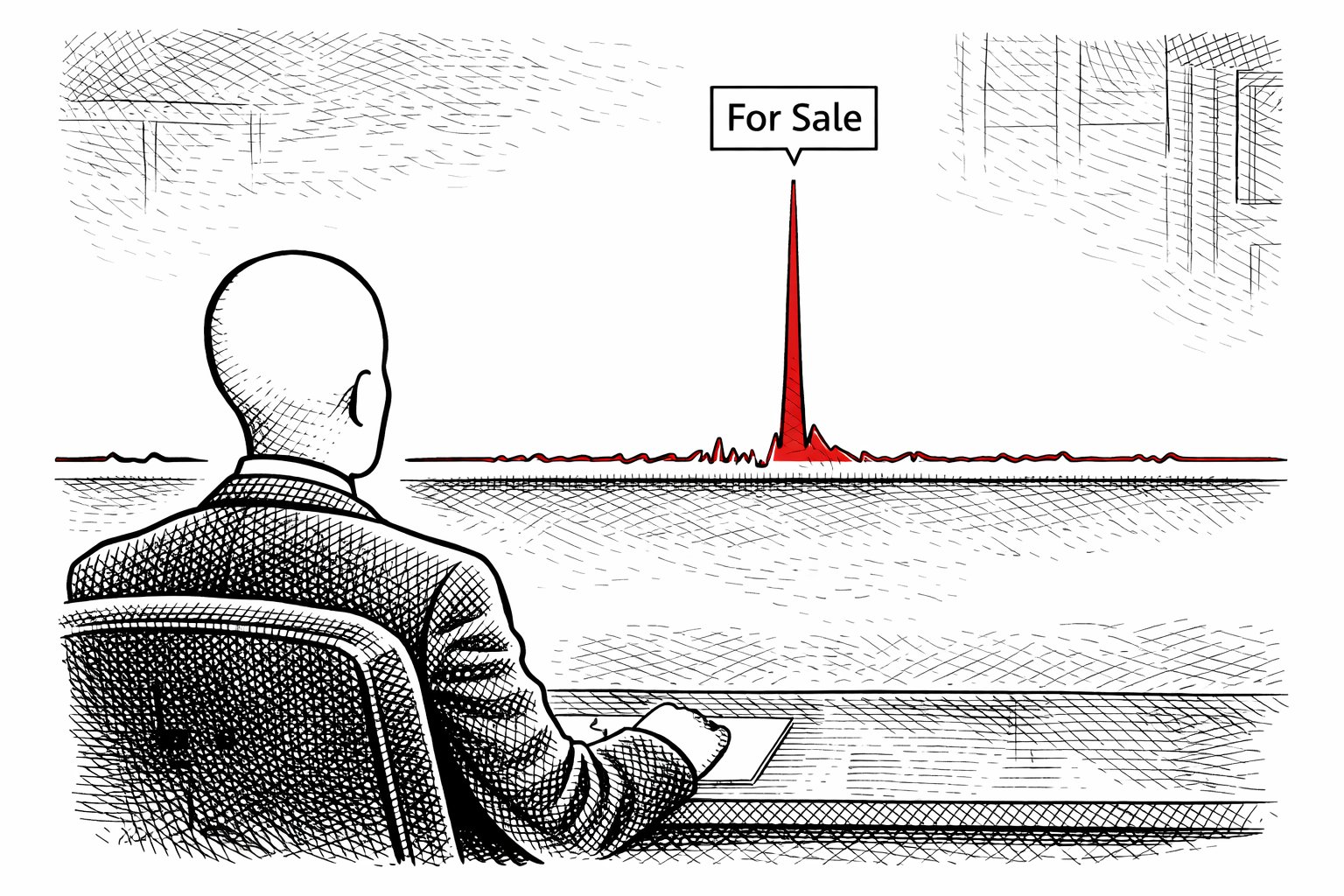

The Takeover Spike as Signal

The most analytically significant episode in MANU's price history is the 2022–2023 takeover period. In November 2022, the Glazer family announced they were exploring "strategic alternatives" including a potential sale. From an approximate price of $12 in early November 2022, the stock more than doubled within three months.18 By February 2023, the enterprise value of the club including net debt had reached $5.2 billion.18 The all-time closing high of $26.84 was reached on 16 February 2023, coinciding precisely with the Raine Group's first-round bid deadline – at which point the stock jumped a further 10% in a single session.20

This movement had no relationship to operational performance, revenue growth, or footballing results. Manchester United had lost to Bournemouth 1–0 on 11 November 2022, the week before the sale announcement. The price spike was the market's unambiguous assessment of one thing: the value of removing the existing ownership structure. When Sheikh Jassim withdrew from the bidding process in October 2023, the stock retreated materially from its February highs.21

In December 2023, Ratcliffe's INEOS acquired a 25% stake at $33 per share – a price representing a substantial premium to the prevailing public market valuation of the same equity.22 Sportico subsequently reported that more than two-thirds of Ratcliffe's share purchases went to equity held by the Glazers, meaning the family received approximately $1.18 billion – "around double what the common stock of the team was worth" at prevailing market prices.30

Glazer Share Sales, 2012–2023

The Glazer family conducted a series of secondary share sales through the NYSE between 2012 and 2021. In each case, the proceeds were received exclusively by the selling Glazer family members; no proceeds from secondary sales flowed to Manchester United Football Club.29

| Date | Shares sold | Price | Proceeds (Glazers) | Club proceeds |

|---|---|---|---|---|

| Aug 2012 (IPO) | 8.33m Class A | $14.00 | ~$116.7m | $0 |

| May 2014 | 12.0m Class A | $17.00 | $200m | $0 |

| Aug 2017 | 4.3m Class A | $17.00 | $73m | $0 |

| Mar 2021 | 5.0m Class A (Avram) | ~$20.00 | ~$100m | $0 |

| Oct 2021 | 9.5m Class A (Kevin & Edward) | $17.50 | ~$161m | $0 |

| Total (2012–2021) | ~39.1m shares | — | ~$650m+ | $0 |

| Sources: Sportico (SEC filings)24; Bloomberg28; Sportico sale timeline.25,26,27 Sportico total share sale proceeds figure to early 2023: $705m. 2021 Avram sale price is approximate. | ||||

By early 2023, Sportico reported that the Glazer family had collected $705 million in share sale proceeds, $573 million in dividends, and $41 million in fees and a forgiven loan from the club since 2005 – a total of approximately $1.32 billion, derived from SEC filings.29 Swiss Ramble estimated total Glazer extraction at approximately £1.6 billion including share sales.29

Shareholder Returns: The Benchmark Problem

| Period | MANU total return | S&P 500 (approx.) | Gap | Source |

|---|---|---|---|---|

| IPO to 2025 (~13yr) | +17.21% (+1.23% ann.) | ~400%+ (~13.5% ann.) | −12.3pp per year | 13,31 |

| 10yr (Mar 2015–Mar 2025) | −3.36% (−0.34% ann.) | ~200%+ (~11–12% ann.) | Negative vs positive | 15 |

| 5yr (to 2025) | ~−8.0% | ~+85% | Substantial | 16 |

| 1yr (Apr 2025–Apr 2026) | +43.08% | +14.8% | +28pp (vs market) | 17,32 |

| Note: Short-term outperformance (1yr) partly reflects recovery from depressed 2024 lows and renewed ownership speculation. Medium and long-term returns remain substantially below broad market benchmarks. | ||||

The 1-year figure as at April 2026 shows MANU outperforming the broad market. That 43% 1-year return requires context: it follows a period in which the stock traded as low as $12.05 (52-week low as of early 2026), and occurs against a backdrop of renewed takeover and stadium-redevelopment speculation.17 The 3-year total return of 23% is a more neutral indicator of the underlying trend.17

The valuation gap

Throughout the stock's history, the enterprise value implied by private market transactions has consistently exceeded the public market capitalisation. Sportico valued United's enterprise value at approximately $5.95 billion in early 2023 at the height of the takeover process.33 The public market cap over the same period was approximately $3.0–3.8 billion. Ratcliffe's transaction at $33 per share in December 2023 implied a full-club value of approximately $5.4 billion, excluding debt.22 Public Class A shareholders, who hold no governance rights and receive no regular dividend, have never captured this control premium in the public market price.

Summary

Manchester United's NYSE listing since August 2012 constitutes one of the least rewarding publicly traded large-cap sports investments of its era. Against an S&P 500 index that grew at approximately 13.5% annualised over the same period, MANU delivered approximately 1.23% annualised, with a 10-year total return that was negative even including dividends reinvested.

The price history is dominated by a single episode – the 2022–2023 takeover process – during which the stock doubled. That movement was not a product of revenue growth, improved sporting performance, or operational change. It was the market's valuation of the probability that the Glazer family would sell. When that probability declined, the stock declined with it.

The structural design of the listing – dual-class shares denying public holders governance influence, no regular dividend, Cayman Islands incorporation chosen in part to avoid London's shareholder protection rules, and repeated secondary sales in which proceeds flowed exclusively to the Glazer family – established from the outset that public shareholders held economic exposure without ownership rights. The IPO was priced below its target range on its first day. Thirteen years later, the gap between the public market price and the control-transaction price remained substantial. What public shareholders have owned throughout is not a proportionate stake in Manchester United's enterprise value. It is a sentiment instrument that rises when the Glazers look likely to leave.

Key Definitional Distinctions

Class A shares are the publicly traded shares available on the NYSE under ticker MANU. Each carries one vote. They are not convertible into Class B shares.

Class B shares are held exclusively by the Glazer family (and, following conversion, by INEOS). Each carries ten votes. Class B shares can be converted into Class A shares at any time by the holder.

Market capitalisation (market cap) is the public share price multiplied by total shares outstanding. It reflects the value the market assigns to the entire equity. Enterprise value is market cap plus net debt – the theoretical total acquisition cost. Throughout MANU's listing history, private-market enterprise value estimates have consistently exceeded the implied public market enterprise value.

Secondary share sale refers to a transaction in which an existing shareholder sells their own shares to new buyers. Proceeds go to the seller, not the company. All Glazer family share sales after the IPO were secondary sales; the club received no proceeds.

References

- 1.Manchester United IR (2012). Investor FAQs. ir.manutd.com

- 2.CNN Money (2012). Manchester United IPO prices below range. cnn.com

- 3.CNN Money (2012). Manchester United raises $233 million in IPO. cnn.com

- 4.SEC EDGAR (2012). Manchester United plc Form 424B4 – IPO Prospectus. sec.gov

- 5.France24 (2012). Manchester United to list on New York Stock Exchange. france24.com

- 6.IBTimes UK (2017). Manchester United shares – for devout fans and signature stock hoarders only? ibtimes.co.uk

- 7.Manchester United IR (2024). Investor FAQs – voting rights as at 18 December 2024. ir.manutd.com

- 8.CFA Institute (2012). Manchester United's IPO: Yellow Card. cfainstitute.org

- 9.CBS News / Morningstar (2012). No win in the Manchester United IPO. cbsnews.com

- 10.TradingView (2024). MANU Stock Price and Chart – NYSE:MANU. tradingview.com

- 11.MacroTrends (2024). Manchester United – 14 Year Stock Price History | MANU. macrotrends.net

- 12.TradingView (2024). MANU all-time low $10.41, 11 July 2022. tradingview.com

- 13.WallStreetZen (2025). Manchester United Stock Price Today (NYSE: MANU). wallstreetzen.com

- 14.StockAnalysis.com (2026). Manchester United (MANU) Market Cap & Net Worth. stockanalysis.com

- 15.HistoricalStockPrice.com (2025). MANU Historical Stock Prices. historicalstockprice.com

- 16.ValuSense.io (2025). MANU Rating. valuesense.io

- 17.Simply Wall St (2026). Manchester United Stock MANU Valuation Check. April 8, 2026. simplywall.st

- 18.Sportico (2023). Manchester United Sale Timeline. sportico.com

- 19.Netcials (2024). Manchester United (MANU) – 6 Price Charts 2012–2024. netcials.com

- 20.Sportico (2023). Manchester United Sale Timeline – Feb 2023 bid deadline. sportico.com

- 21.Sportico (2023). Manchester United Sale Timeline – Sheikh Jassim withdrawal Oct 2023. sportico.com

- 22.Sky Sports (2023). Manchester United takeover: Sir Jim Ratcliffe completes deal to purchase 25 per cent. skysports.com

- 23.StockAnalysis.com (2026). Manchester United Market Cap History 2012–2025. stockanalysis.com

- 24.Sportico (2023). Manchester United a Billion-Dollar Win for Glazers. sportico.com

- 25.Sportico (2023). Sale Timeline – May 2014 secondary sale. sportico.com

- 26.Sportico (2023). Sale Timeline – Aug 2017 secondary sale. sportico.com

- 27.Sportico (2023). Sale Timeline – Mar 2021 Avram Glazer sale. sportico.com

- 28.Bloomberg (2021). Manchester United Stock Drops After Glazers Offer Stake Sale. bloomberg.com

- 29.Sportico (2023). Manchester United a Billion-Dollar Win for Glazers Even Before Impending Sale. sportico.com

- 30.Sportico (2025). Man United's Other Owners Profit as Ratcliffe Sees $700 Million Loss. sportico.com

- 31.FinanceCharts (2025). Manchester United (MANU) Performance History & Total Returns. financecharts.com

- 32.Simply Wall St (2026). Manchester United (NYSE:MANU) – Stock Analysis. simplywall.st

- 33.Sportico (2023). Premier League Team Valuations 2023. sportico.com

- 34.IBTimes UK (2017). Manchester United shares – for devout fans and signature stock hoarders only? (Andy Green / MUST commentary). ibtimes.co.uk

- 36.CFA Institute (2012). Manchester United's IPO: Yellow Card – GAAP/quarterly filing note. cfainstitute.org

- 37.TradingView (2026). MANU beta coefficient 0.61. tradingview.com